The Philippine property market has always moved in cycles—rising with confidence, correcting with caution, and recalibrating in the face of external shocks. Over the past three decades, average capital values have broadly tracked GDP growth swings.

From the Asian Financial Crisis and Global Financial Crisis to Covid-19, the pattern is consistent: volatility is inevitable, but dislocation is temporary. This year, the Department of Budget and Coordination Committee (DBCC) is projecting economic growth to be between 5.0 percent and 6.0 percent, signaling a softer yet still positive expansion environment for Philippine real estate. The question today is not whether disruption will occur—but how deep and prolonged it will be.

One of the most immediate transmission channels of a Middle East conflict to the Philippine property sector is through remittances. In 2025, remittances from Middle East countries reached approximately USD 6.5 billion, accounting for about 18 percent of total inflows. These flows have grown at a steady 3.9 percent CAGR from 2020 to 2025, highlighting the sustained dependence of Filipino households on overseas income. Saudi Arabia, the UAE, and Qatar remain the largest contributors, collectively accounting for a substantial share of these inflows. Any escalation in regional tensions could disrupt employment conditions, remittance flows, and ultimately housing demand—particularly in end-user driven markets.

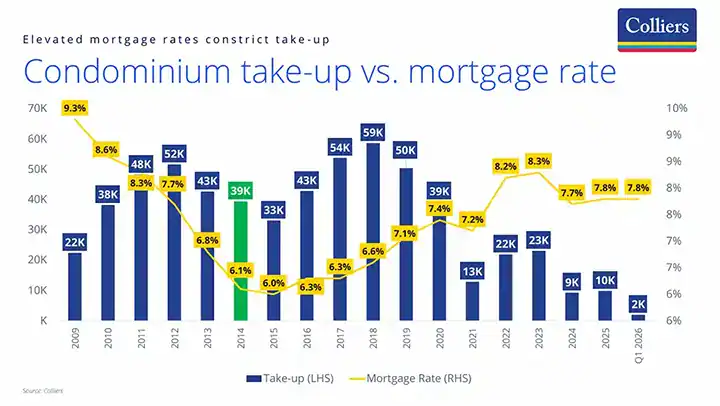

Pricing dynamics in the residential sector reveal an emerging imbalance. Colliers Philippines has noted that pre-selling condominium prices have increased by an average of 8 percent annually, outpacing both personal income growth at 5 percent and remittance growth at 3 percent over the same period, according to latest government data. This widening affordability gap suggests that even in the absence of external shocks, demand could begin to normalize. Historical data shows pre-selling prices rising from about 101,000 per sqm in 2017 to nearly 190,000 per sqm by 2025, underscoring the sharp escalation in entry-level costs. A potential slowdown in remittance inflows could therefore accelerate a correction in take-up, particularly among OFW-dependent buyers.

On the supply side, construction costs are once again under pressure, largely driven by movements in global oil prices. Developers and contractors are feeling the pinch of elevated construction material prices. All over the market we see residential projects being put on hold as surging prices are squeezing contractors’ profits.

From oil shocks to mortgage rate spikes, the Philippine property cycle is once again being stress-tested. History reminds us that while volatility can dent sentiment, it doesn’t exactly hamper structural demand anchored on urbanization, demographic growth, and sustained capital formation. Colliers Philippines believes that what we may be entering is not a downturn, but a disciplined phase—where buyers become more selective, developers more strategic, and pricing more reflective of real purchasing power and end-user demand.

For developers and investors, this is a moment to recalibrate—not retreat. Product mix diversification, right-sized unit offerings, and flexible payment schemes will be critical levers to sustain take-up across the Philippines. Meanwhile, markets outside the traditional core—particularly those supported by infrastructure and domestic employment hubs—may provide pockets of resilience. As we highlight at Colliers Philippines, the property sector is unlikely to collapse under pressure; instead, it will adjust, reprice, and regain equilibrium. Cycles may bend confidence, but they rarely break conviction.

The article was originally published in Business Mirror and written by Joey Roi Bondoc.

If you like this article, share it on social media by clicking any of the icons below.

More Stories

‘Flight to the South’ benefits green developer Arthaland

Empire East Highland City takes shape as flagship future-ready township

Reytech returns to Philconstruct Manila 2026