A REAL estate service firm affirmed the dominance of the mid-income segment in the pre-selling market, capturing 70 percent of the net demand and posting an 8 percent year-on-year (YoY) increase in net take-up in 2025.

During the media briefing on Feb. 3, Colliers Philippines’ Research Director Joey Bondoc credited this “renewed strength” in the mid-income condominium segment, priced between P3.6 million and P12 million, to increased developer competition, including new launches, stronger net take-up, and aggressive Ready-for-Occupancy (RFO) promotions.

These factors resulted in reduced inventory life from “double-digit” years to below 8 years, or 95 months. This marks a significant drop, Bondoc said, from a high of 13.4 years recorded in the second quarter of 2025.

“Developers really ramped up their RFO promo offerings and lease-to-own terms in the market. The fact that developers did that means that they are probably cognizant of this figure, which resulted in a tremendous decline in unsold inventory life,” he said.

The firm also noted that the luxury market — holding a steady 3 percent unsold inventory — is on the rise, as more premium residential projects are slated for turnover in 2026 and 2027. Bondoc referred to this trend as the “influx of the lux,” or condominiums priced at P20 million and above. Of the total demand of turnover in Metro Manila, this segment is expected to account for 22 percent in 2026 and rise sharply to 62 percent in 2027.

Notable luxury projects clustered in Makati CBD and Fort Bonifacio include Eluria by Arthaland (P160 million per unit); Aurelia Residences by RLC Residences and Shang Properties (P140 million per unit); Parkford Suites by Alveo Land (P50 million per unit); The Estate by SMDC and Federal Land (P108 million per unit); and Seasons Residences-Fuyu by Federal Land and Nomura (P35 million per unit).

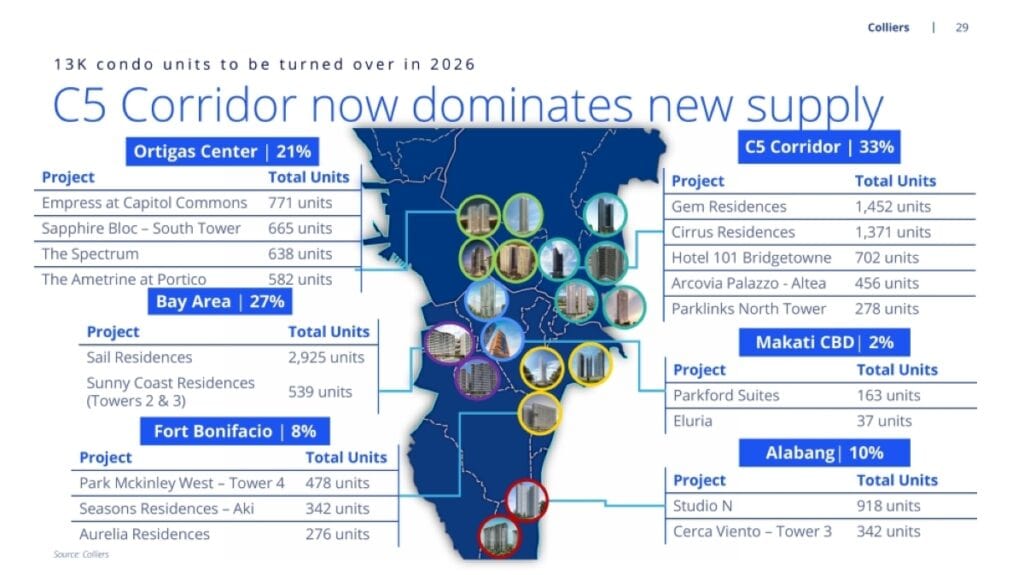

In terms of overall supply, 13,000 units are scheduled for completion this year — effectively doubling last year’s volume and marking the highest level in nine years. About half of this supply is located in Fort Bonifacio and the Bay Area. Meanwhile, the C5 corridor is gaining ground, already accounting for 33 percent of new supply across Metro Manila.

A growing corridor

“In 2026, the C5 corridor — a relatively newer business district and a former industrial warehousing zone converted into a master-planned community — will deliver a third of the completion for the rest of 2026,” Bondoc said, noting its significance because “many developers have their respective townships along the C5 corridor.”

The Bay Area, with 27 percent of new supply in 2026, follows closely behind the C5 Corridor. However, despite the expanding supply in this submarket, Bondoc expressed concern over the persistently elevated vacancy levels in the area. “We are projecting vacancy to hover between 55 and 57 percent, and because of sizable completion in 2027, vacancy will stay elevated,” he said.

Outside Metro Manila, Bondoc said developers are briskly pursuing differentiation strategies in large-scale estates in Pampanga (Hann Reserve by Hann Development and Centrala by Ayala Land); Ilocos (Ilocandia Coastown by Megaworld); Batangas (Lialto by Megaworld and Arillo by Ayala Land); Cavite (Villar City by Vista Land and Riverpark by Federal Land); Bacolod (Saludad by Phinma Properties); and Davao (Ascenda by Ayala Land).

According to Bondoc, builders are pivoting and “really differentiating their projects” by incorporating features such as golf courses, active lifestyle amenities, family-friendly institutions like schools and hospitals, and large commercial lots in their master-planned communities.

One key differentiator Bondoc highlighted is the offering of commercial lots within these integrated developments.

“When you have master-planned communities, you have residents who will need retail establishments and support facilities, even hotels and convention halls. To build those, you need commercial lots,” he said.

To address this demand, Bondoc noted that developers in areas outside the National Capital Region (NCR) are offering “massive sizes” of commercial lots. Lot sizes average 2,000 sqm in Cebu, priced at P293,000 per sqm; 1,400 sqm at P110,000 per sqm in Laguna; 1,400 sqm at P108,000 per sqm in Cavite; and 1,600 sqm at P69,000 per sqm in Pampanga.

The article was originally published in The Manila Times and written by Michele T. Logarta.

If you like this article, share it on social media by clicking any of the icons below.

More Stories

Vista Residences Ready-to-Move Deals: High-Rise Homes for RFO Buyers and Investors

Developer financing props up condo market, analysts say

Anko boosts presence in local retail sector