SURGING interest rates and regulatory scrutiny are causing distress for builders and creditors in Asian economies from South Korea to Vietnam, highlighting the breadth of housing woes in a region overshadowed by China’s crisis.

While aggressive monetary tightening and the pandemic have had a more pronounced impact on commercial property in the US and Europe, it’s residential housing that is under more strain in Asia. One of the worst hit nations, South Korea, saw the steepest home price slump in 25 years while a construction firm’s repayment struggle has rekindled fears of repeating the credit market turmoil in 2022.

“Countries that had high consumer debt or balance sheet burden will be areas that you want to focus on,” said Kheng Siang Ng, head of Asia Pacific fixed income at State Street Global Advisors. “Korea is one of them. Housing markets have been softening.”

Here are some places where property market risks have the potential to boil over in 2024:

SOUTH KOREA

Korea’s property market is showing the most strain after China in the region, with prices in 2023 falling by the most in a quarter of a century after years of growth. The weakness is the direct outcome of moves by the Bank of Korea — the first major Asian central bank to kick off the current monetary tightening cycle in 2021 — to push its policy rate to a 15-year high.

Turning the weakness into a crisis was a theme-park developer’s debt blowup in late 2022 that snowballed into the worst meltdown in the country’s credit market since the global financial crisis. While a suite of government rescue measures stabilized the situation, an engineering and construction company’s request to reschedule debt in late December prompted authorities to pledge more support.

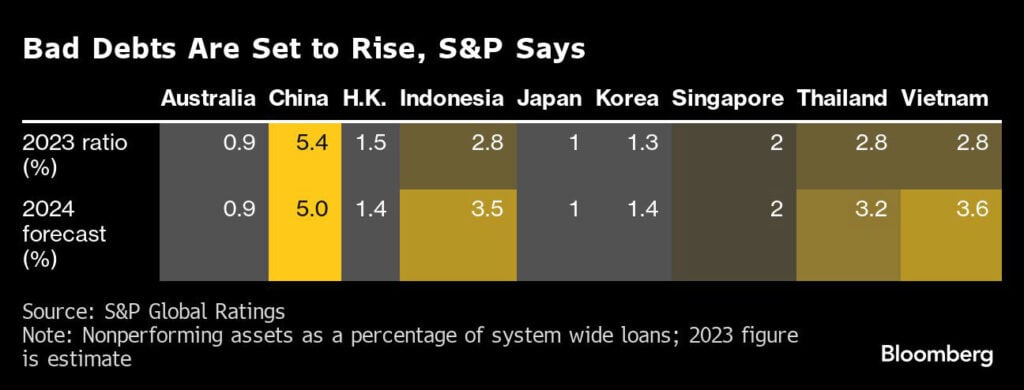

Bad debts for both households and companies are piling up and the Bank of Korea said risks related to project financing debt — a type of security used to finance construction that triggered the 2022 crisis — are likely to increase next year. Even so, officials say the country’s financial system will generally remain stable.

The “potential restructuring of real estate project financing loans from the middle of 2024 following the election in April 2024 could raise volatility in the short-term money market at least temporarily,” said Citigroup, Inc. economist Kim Jin-Wook.

INDONESIA

The local central bank’s most aggressive rate hikes since 2005 put heavily indebted home builders such as PT Lippo Karawaci and PT Agung Podomoro under pressure, as it crimped household purchasing power. A weak currency made matters worse, by increasing the cost of servicing their soon-to-mature dollar debt, forcing them to resort to asset sales to raise cash.

Fitch Ratings said at the end of November that “some kind of default is probable” on Agung Podomoro’s $132-million bond due in June 2024 after it has canceled an offer to buy back part of the unsecured notes. Refinancing risks for Lippo Karawaci, Lippo Group’s Indonesia unit, also are rising, according to Fitch, which downgraded the firm’s dollar note due in January 2025 to CCC+ in November.

But the prospect of an end to Indonesia’s policy tightening is giving dollar-denominated property notes an uplift, as investors anticipate an improvement to real estate demand.

Fitch has predicted a recovery in local corporate bond sales, citing increased refinancing needs and a more supportive economic environment. Borrowers are expected to continue to prefer shorter-tenor issuance in 2024, as there is higher demand for short-term notes amid rate uncertainty, Fitch said.

VIETNAM

The government’s ambitious anti-graft campaign upended Vietnam’s property sector already plagued by oversupply, impeding corporate bond issuance that triggered a liquidity crunch and missed payments by borrowers. But regulatory interventions and multiple interest rate cuts have slowed the downward spiral.

“Vietnam’s real estate market has had an extraordinarily challenging year, but we believe the worst of the downturn has now passed,” Michael Kokalari, chief economist at VinaCapital Group Ltd., wrote in a report. “Mortgage rates peaked at as high as 16% at some banks in early 2023 but subsequently dropped dramatically.”

Still, signs of trouble remain. Some banks have thin capital buffers and some have high exposure to real estate, according to Sue Ong, credit analyst at S&P Global Ratings.

The poster child of the property woes is Novaland Investment Group Corp., one of the country’s biggest developers, notable for having a US-currency bond. The company agreed a maturity extension on holders of its $300-million convertible note, after an interest payment failure in July.

While the price of the note picked up on news the firm had struck a deal with creditors, the note is still indicated at 36 cents on the dollar, according to Bloomberg-compiled data. That’s a deeply distressed level showing low investor expectations for full debt recovery.

Perpetual dollar bonds issued by several of the city’s developers suffered their worst selloff in years in August, amid worries about soaring financing costs and the spillover impact of China’s real estate woes. Leading the declines were New World Development, Co. — one of Hong Kong’s most indebted developers. It’s debt underperformed industry peers this year.

Behind investors’ nervousness is a local property slump that saw the city’s home prices drop to the lowest in almost seven years. Revenues from office buildings and retail space have also weakened following three years of stringent COVID curbs and the Federal Reserve’s historic monetary tightening.

Demand was so depressed that Hong Kong developers were forced to cut home prices significantly, a tactic they hadn’t deployed for years, while banks struggled to lure buyers for foreclosed homes at equally deep discounts.

“We are cautious about developers in Hong Kong with large exposure to residential and commercial properties in lower tier cities in mainland China as well as those with large office portfolios outside prime districts due to the elevated vacancy rate and continued negative rental revisions,” said Zerlina Zeng, senior credit analyst at Creditsights. “We continue to underweigh Hong Kong developers with higher leverage due to the rising HKD funding costs, which would persist in 1H24.”

AUSTRALIA

It’s a slightly different form of property stress in Down Under, where the Reserve Bank of Australia’s (RBA) aggressive tightening cycle has raised concerns over households’ ability to stomach higher interest rates.

The International Monetary Fund (IMF) has indicated the country is liable to feel the effect of higher borrowing costs, at a time when a large chunk of home loans fixed at record-low rates during the pandemic are set to be rolled over to higher, floating rates. In Australia, more than 50% of mortgages have variable rates, according to the IMF.

The RBA warned in October that a small but growing number of households were in the early stages of financial stress. About 14% fixed-rate borrowers expected to face a rise in mortgage payments of more than 60% once their maturities expire, it said.

Data from the Australian Prudential Regulation Authority on banks’ residential property exposure show new non-performing loans climbing to a three-year high though they still remain relatively low. — Bloomberg

If you like this article, share it on social media by clicking any of the icons below.

Or in case you haven’t subscribed yet to our newsletter, please click SUBSCRIBE so you won’t miss the daily real estate news updates delivered right to your Inbox.

The article was originally published in Business World.

More Stories

Vista Land Celebrates 50 Years with Sandiwa: An Event Honoring Leadership, Legacy, and the Filipino Dream of Homeownership

Vista Land Celebrates Love Month in Ilocos Region

Vista Land Bridges Cebuano Heritage and Progress with Valencia by Vista Estates