Cushman & Wakefield’s 2024 Asia Pacific Office Outlook provides supply, demand, vacancy and rent data forecasts for cities in Australia, China, India, Indonesia, Japan, Korea, Malaysia, the Philippines, Singapore, Thailand and Vietnam.

REGIONAL OVERVIEW

Key Messages:

- Inflation, though largely improved, remains above target bands in most markets across the region; a ‘higher for longer’ interest rate scenario is anticipated.

- Asia Pacific economic growth is expected to slow but to remain in positive territory (3.5% to 4.0% real average annual growth) in 2024.

- Despite a weaker economic outlook, regional office demand is forecast to reach pre-pandemic levels in 2024—but above average levels of new supply will drive vacancy higher1.

- Rental growth is forecast to remain flat in 2024 before slowly accelerating from 2025.

- Newer, high-quality buildings are likely to outperform given the ongoing flight to quality.

Against a volatile economic backdrop, the Asia Pacific office market remains steadfast and continues to grow. Approximately 50 million square feet (msf) of Grade A office stock was absorbed across the region’s top 25 cities during the first nine months of 2023, with a further 12 msf expected in the final quarter. Annual office demand in 2023, forecast at 62 msf, is an 11% improvement on last year’s 55 msf.

New supply in 2023 will total 109 msf, outstripping demand and causing vacancy to tick upwards to 17.6% from 16.1% in 2022. Rental growth has subsequently slowed and is likely to be down around 0.5% on a weighted average basis.

The outlook remains broadly skewed to the positive. Demand is forecast to increase to 83 msf in 2024 and to 87 msf in 2025, which would match pre-pandemic performance. However, waves of new supply are also expected, with nearly 235 msf of completions forecast over the next two years to place further upward pressure on vacancy, which is now expected to peak at 18.4% in 2024 and then hold steady through 2025. This will keep downward pressure on rents which are likely to remain flat in 2024, at the weighted regional average level, before slowly accelerating from 2025. Accordingly, the window of opportunity remains open for occupiers over the near term2.

ECONOMIC CONTEXT

While uncertainty abounds globally, there are some reasons for cautious optimism.

Inflation

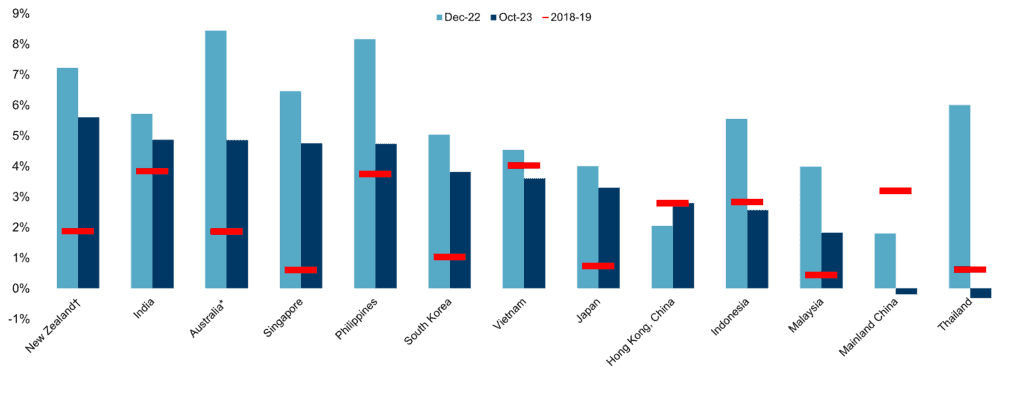

While inflation remains elevated in most economies, it is well down on the peaks experienced in late-2022. This decline has been driven by several factors including a downturn in fuel and energy costs, as well as base effects. Persistent inflation in other categories, including food, is keeping inflation above many central banks’ target bands. Many economies have also experienced significant currency weakening, which has fuelled import costs. While challenges remain, central banks are generally deep into their hiking cycles. Forecasts on when interest rate cuts remain a source of debate, but consensus is they are likely to be after mid-2024 for most economies.

Figure 1: CPI Change (% y-o-y) for select markets

Source: Moody’s Analytics

Labour

Labour markets have mostly remained remarkably resilient so far during this rapid hiking cycle. Unemployment in 11 of the region’s 14 major economies is forecast to end 2023 at a rate lower than the 5-year pre-pandemic average. The remaining three economies – Thailand, Indonesia and mainland China – will be above their five-year averages by 26 basis points at most. Almost 11 million jobs are estimated to have been created in Asia Pacific in 2023, with 3.7 million of them in the office sector. The job creation forecast for 2024 is 8 million jobs, including 2.1 million office jobs.

Trade

Economies around the world have slowed as businesses and households alike have reined in expenditure in response to interest rate increases. Slowing demand for products in North America and Europe has negatively impacted trade in Asia Pacific, which remains well below recent peaks—although the decline appears to have stabilised in Japan, Thailand and Vietnam.

Growth

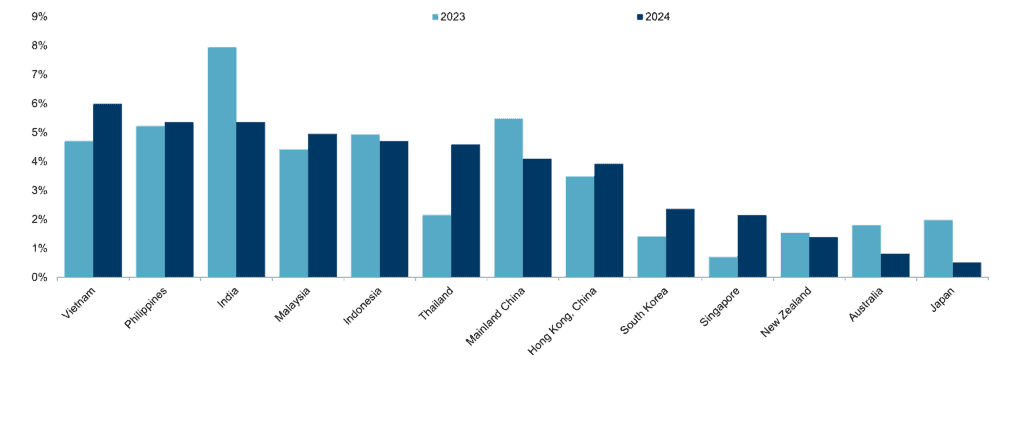

Asia Pacific growth is forecast between 3.5% and 4.0% in 2024, compared to a forecast 4.5% in 2023. Although slowed, this growth outlook remains stronger than other regions. While both North America and Europe have proven more resilient in 2023 than initially forecast, 2024 is likely remain challenging: euro zone growth is forecast at 0.9% and US growth at -0.3%.

Growth trajectories within Asia Pacific vary, most evidently between advanced and emerging economies. Vietnam, Philippines, India and Malaysia are forecast to lead the way. India has been a leader amongst the world’s larger economies in 2023, supported by infrastructure development, strong domestic consumption and foreign investment. The Philippines has also benefited from strong domestic consumption and government expenditure. Indeed, much of Southeast Asia is entering a period of strong growth, fuelled in part by manufacturers’ increasing attraction to the sub-region and consequent foreign direct investment. Tourism, which remains 25% below pre-pandemic levels in Asia Pacific, could provide further support for growth, especially in Thailand.

The outlook for the region’s advanced economies is more mixed. Singapore is forecast to rebound after a difficult 2023 as trade, especially demand for electronics components, starts to recover; this should also benefit South Korea. China’s outlook is a little more undetermined. China’s exposure to global export demand, soft domestic consumption and a tempered property market are all issues at hand in the market. One mitigating factor is that monetary policy continues to be eased.

Australia and Japan are likely to trail the region. High interest rates in Australia are curtailing domestic consumption given the greater adoption of variable mortgage rates and so more meaningful growth is not expected until the central bank starts its interest rate cutting cycle, which it forecasts is not due until 2025. In Japan, minor adjustments to the short-term negative interest rate are expected in late-2024 following some relaxation of yield curve controls in 2023. Whether real wage growth can be sustained remains a key issue to watch.

Figure 2: Real GDP growth (% average annual) for select markets in 2023 and 2024

OFFICE OUTLOOK

Supply

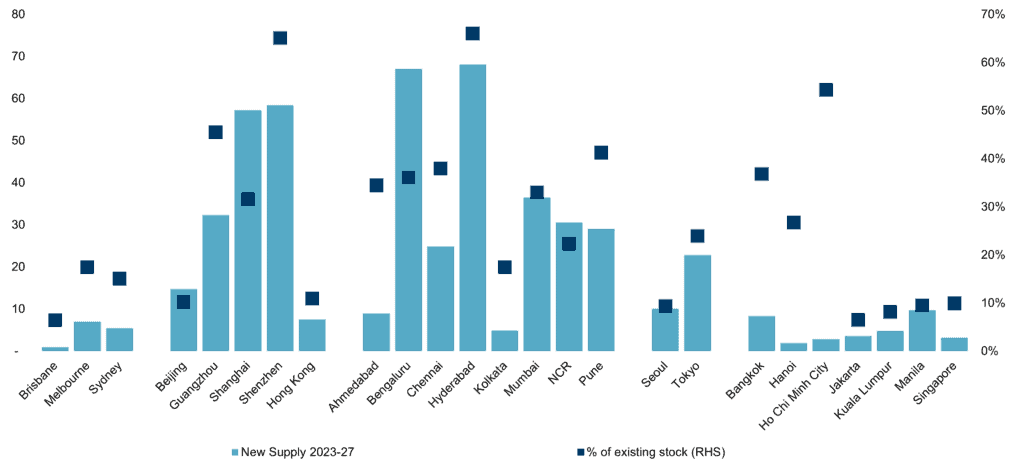

The region has entered a period of above average new supply, which is expected to continue through to 2025 before starting to ease. Of the 25 markets forecast, 16 will welcome more supply in 2023–25 than 2017–19 as pandemic-delayed construction continues to enter the market. Collectively, cities in India account for almost half – 168 msf – of the forecast new supply in 2023–2025.

Unsurprisingly, the region’s largest office markets have the largest supply pipelines over the full 2023-27 forecast horizon. Hyderabad, Bengaluru, Shanghai and Shenzhen are all expecting over 55 msf to be brought to market by 2027, which represents from 32% to 66% of existing stock and highlights not only how large these markets have become, but their continuing rapid growth.

In contrast, supply is relatively constrained in Brisbane, Jakarta, Seoul and Singapore. Each of these markets have supply pipelines through to 2027 that total less than 10% of existing stock. In Brisbane, there are several years where no new supply is expected, whereas the other markets more reflect a “little and often” approach.

Figure 3: New supply in 2023-27* (msf) and as a percentage of existing stock in 2023

Demand

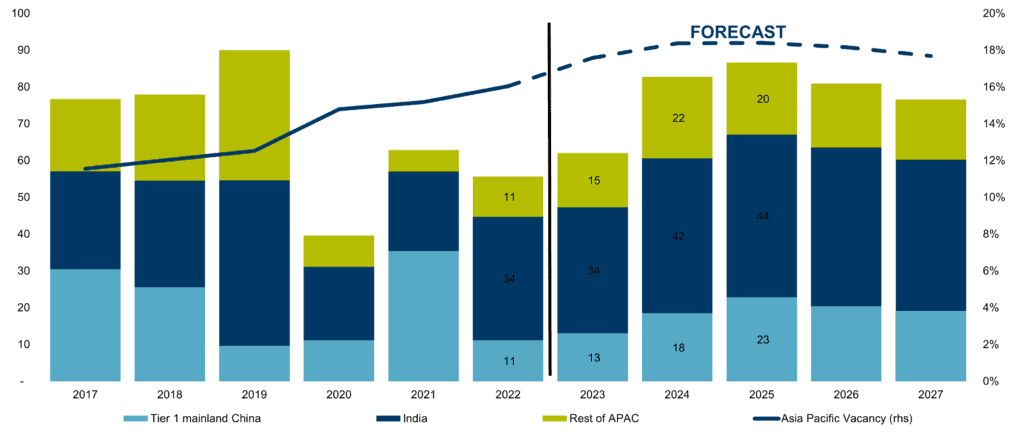

From a demand perspective, the top eight Indian real estate cities have led the region in net office absorption over the past 18 months, fuelled by both expansion of domestic companies and the ongoing growth of global capability centres, predominantly in technology-focussed cities. This leading position is not expected to be challenged over the forecast horizon, with net absorption forecast to average approximately 40 msf per annum, equivalent to around 52% of the regional total.

The recovery in mainland China’s tier one cities is also expected to continue. Office demand in these four cities (Beijing, Shanghai, Guangzhou and Shenzhen) is expected to end 2023 at a little over 13 msf, a 20% improvement on 2022, then accelerate to almost 18 msf in 2024 and remain around 20 msf per annum for the remainder of the forecast period.

Some markets across Southeast Asia are also forecast to experience a strong uptick in demand. Kuala Lumpur and Manila, with their expansive national economic growth outlooks, stand out, while Singapore is likely to continue its steady performance as its economy rebounds.

Elsewhere, Tokyo is starting to emerge from a comparatively slow 2021–22 period, with demand in 2024 forecast at 5.3 msf—the highest level of net absorption in several years. Supply-led demand, however, remains a key driver as tenants relocate to higher quality buildings and/or locations.

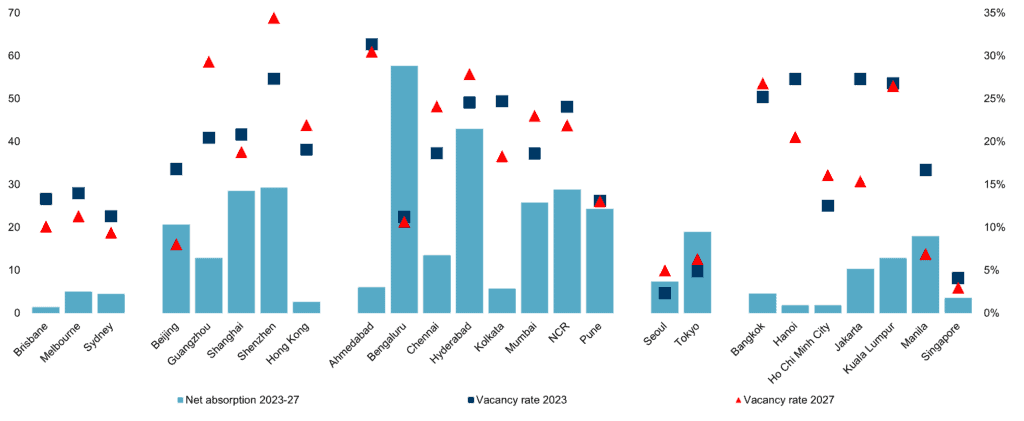

Figure 4: Regional annual grade A office net absorption (msf) and vacancy rate by broad geography*

Source: Cushman & Wakefield

This remains an important issue across the region. Recent analysis has highlighted the importance of building location and quality in occupier decision-making . Factors such as sustainability and technology accreditation are becoming increasingly important, yet adoption of both remains at relatively low levels across Asia Pacific. Accordingly, demand is likely to be further bifurcated or even trifurcated, and led by best-in-class buildings in good locations, and/or by those buildings with re-positioning potential.

Vacancy

Despite the positive outlook for office demand, vacancy is expected to continue pushing upwards in 2024 as new supply exceeds demand. While approximately half of the markets forecast are expected to experience higher vacancy in 2027 than 2023, the most significant increases are concentrated in just a few markets. Guangzhou’s vacancy rate increased around 600bps in 2023, from 14% to 20%, and is forecast to rise to almost 30% by 2027. A similar situation is seen in Shenzhen, with vacancy rising from 27% in 2023 to almost 35% in 2027. While these are the largest vacancy rate increases, vacancy rates in markets including Hyderabad, Kuala Lumpur and Bangkok are forecast to exceed 25% by 2027. This is primarily driven by new supply, as positive office demand is expected to endure in all these markets. Again, this highlights the importance of truly understanding tenants’ needs when positioning assets within high vacancy markets.

Singapore and Seoul are likely to remain the tightest markets in the region, with vacancy in both remaining below 5%. Neither Tokyo nor Manila is expected to exceed 7% over the forecast horizon (2027). In Australia, vacancy rates are expected to remain stable at around 10%, though this is likely to tighten in Brisbane and Sydney toward the end of the forecast horizon as supply pipelines dry up.

Figure 5: Net absorption (msf) and vacancy rate, 2023-27

Rent

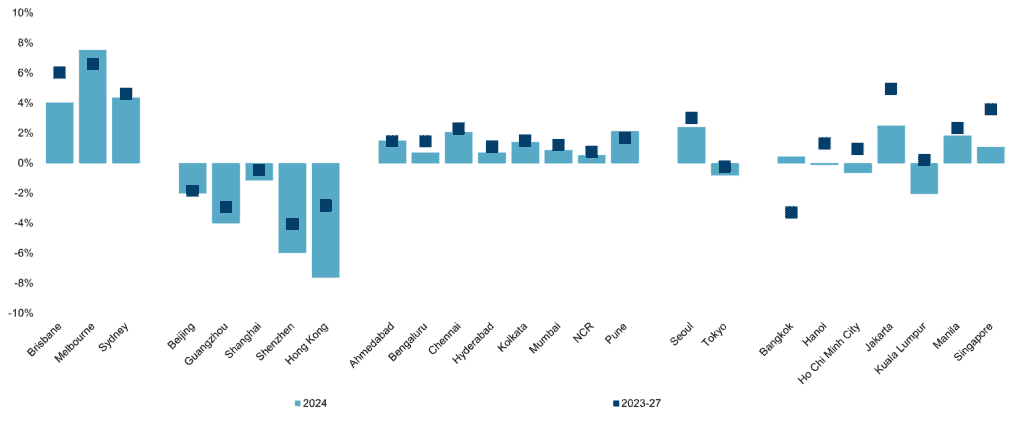

Bringing these factors together suggests that there will be comparatively little upward pressure on rental growth over the near-term at the aggregate level. However, this is not universally true at the local level, and in almost all markets there remains a bifurcation with higher-quality stock likely to outperform the wider market and the the vast majority of poorly located, lower-quality buildings likely to remain under significant pressure.

Sub-regionally, recent performance has been varied. Australian markets have led rental growth across the region in 2023, topped by Brisbane. Together with Sydney and Melbourne, these three markets are forecast to show the strongest growth through to 2027, averaging around 4% to 7% per annum. Jakarta’s forecast rental increase over the same time is similar, though this is predicated on strong growth from 2025 which would need to come to fruition to offset slower growth in the near-term. In Singapore, steady growth of around 4% per annum is forecast from 2025 onwards, fuelled by strong demand, limited supply and already-tight vacancy.

Rental growth elsewhere in the region is more muted. Soft conditions in the near-term remain prevalent across tier one markets in mainland China. Rents in Tokyo are expected to remain flattish with minor downside risk expected until 2027.

Figure 6: Rental outlook by market, 2024 (% y-o-y) and 2023-27 (% per annum)

If you like this article, share it on social media by clicking any of the icons below.

Or in case you haven’t subscribed yet to our newsletter, please click SUBSCRIBE so you won’t miss the daily real estate news updates delivered right to your Inbox.

The article was originally published in Cushman & Wakefield.

More Stories

Vista Land Celebrates 50 Years with Sandiwa: An Event Honoring Leadership, Legacy, and the Filipino Dream of Homeownership

Vista Land Celebrates Love Month in Ilocos Region

Vista Land Bridges Cebuano Heritage and Progress with Valencia by Vista Estates