- Retail and hotels are the fastest-recovering property sectors

- OFW remittances and household spending growth drive retail space demand

- Retail occupancy in Metro Manila at 93% in Q4 ’22, nearing 96% pre-pandemic level

- Metro Manila warehouse rents jumped by 15% half-yearly in Q4 ’22 – highest in Southeast Asia

- 2,692 new hotel rooms expected until 2024 in Metro Manila

- Office sector to show net positive growth in 2023

- Green buildings outperform non-green buildings in occupancy

- Office occupiers eye cities outside Manila such as Iloilo, Cebu, and Clark for their 2nd or 3rd offices

- As tech layoff, inflation, and cost-cutting measures continue globally, companies pivot to the Philippines and India for outsourcing

Santos Knight Frank forecasts a rosy outlook for Philippine property in 2023 as key sectors, including retail, hospitality, industrial, and office, expect a sustained return of demand this year. After a positive Q4 2022 performance, the industry’s recovery is expected to accelerate in 2023, propelled by a resilient and stable economy and by the sustained growth of OFW remittances and household spending, weathering headwinds such as interest rate hikes and inflation.

As markets recover, Santos Knight Frank also believes that the Philippines is now much better positioned to attract investments from overseas, with companies from the U.S. and other countries confident with President Ferdinand Marcos Jr’s administration. President Marcos has generated approximately USD 23.6 billion in investment pledges in 2022 from his overseas trips.

Together with key legislations supporting investments (e.g. the Foreign Investments Act, Public Services Act, and Retail Trade Liberalization Act), the government continues to drum up interest for the country that is crucial for sustained recovery and growth.

Fast-recovering Sectors: Retail and Hospitality

The Philippines’ 7.6% GDP growth in 2022 was already the fastest in four decades, driven by a 6% increase in consumption. This trend supports the robust demand for retail space; mall occupancy level across Metro Manila closed at 93% by the end of 2022. (Mall occupancy was at 96% in Q4 2019 before the pandemic.)

With 2.65 million international tourist arrivals to the Philippines in 2022, the return of travel also comes as hotel construction developments across the country continue. Between this year and 2024, Santos Knight Frank expects approximately 2,692 new hotel rooms to be delivered in Metro Manila alone.

Rick Santos, Chairman & CEO of Santos Knight Frank, comments: “Brick-and-mortar retail and hotels were some of the most severely affected real estate sectors during the pandemic. Now that travel and mobility restrictions have been lifted, we are seeing the resurgence and ‘unfreezing’ not just of market activity but also development and expansion of players in these sectors.”

Office Sector Still a Tenants’ Market

The question of work-from-home setups especially for IT-BPM companies will continue to impact the demand for office space. In early January, PEZA said a total of 452 registered business enterprises involving 1,325 IT-BPM projects were endorsed to the BOI, therefore allowing said businesses to do WFH setups. The deadline of the application for transfer of existing registered IT-BPM businesses from PEZA to the Board of Investments was 31st January, 2023.

The move to allow WFH has enabled IT-BPM companies to find harmony in designing their work setups. In general, Santos Knight Frank predicts that companies in 2023 will re-assess their hybrid work experience, its impact on productivity and employee wellbeing, and adjust their requirements for office space, accordingly.

Morgan McGilvray, Senior Director for Occupier Services at Santos Knight Frank, says: “We expect more leasing activity this year as a result of greater outsourcing requirements from developed economies, the availability of quality office space, and companies adjusting their work setups. While we will continue to see some downsizing of footprints for Philippine headquarter companies, we still expect to see an overall net positive take up in 2023 driven mainly by the BPO sector.”

PEZA-accredited Buildings

The difference in occupancy between PEZA-accredited and non-PEZA-accredited buildings was already nearing parity by the end of 2022. Buildings accredited by PEZA have registered a 16% average vacancy rate versus non-PEZA, which had 19% average vacancy at the end of 2022.

In 2023 and beyond, Santos Knight Frank expects BPO tenants that were once restricted to PEZA-accredited buildings to consider a wider pool of options for their next office space.

A Premium for Green

Green buildings, in general, continue to be more resilient in their occupancy level than do non-green buildings. In fact, LEED-certified office buildings registered an 11% average vacancy and PhP 1,090 average asking monthly lease rate versus 24% vacancy and PhP 942 asking monthly lease rate in non-LEED buildings.

Morgan McGilvray comments: “Corporate multinationals have always looked for high-quality buildings, and we saw a move towards LEED buildings begin about 10 years ago. Now, these same firms often have ESG targets as well, which require them to not only be in green buildings, but also to find landlords that can help the firms achieve sustainability objectives., This trend is called Green Leasing, and we’re already seeing happen in developed markets such as Australia, the U.K, and the U.S.. We expect to see a similar trend reach the Philippines over the next few years.”

Industrial Outlook

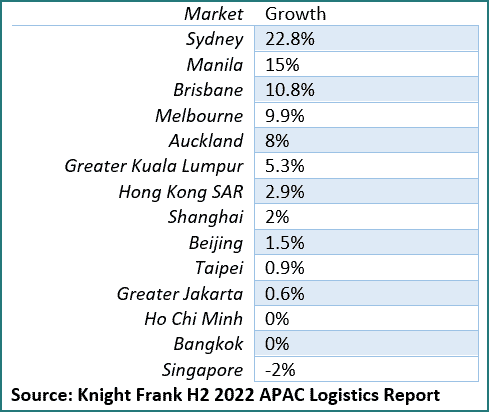

Growth in consumption means favorable demand in the industrial and logistics real estate sector. Although rental growth of warehouses slowed across Asia Pacific to 0.6%, Manila’s warehouse sector registered the highest lease rate growth half-yearly in Southeast Asia at 15%, according to Knight Frank’s H2 2022 APAC Logistics Highlights report. Across the APAC region, Manila had the second fastest, coming only after Sydney (22.8%). Rick Santos comments: “The industrial, logistics, and warehouse sector has always been a bright spot in Philippine real estate. As markets recover from the pandemic, greater activities in construction, manufacturing, and e-commerce industries are driving demand for storage.”

Asia Pacific Logistics Rental Growth Half-Yearly (Q4 ’22 vs Q2 ’22)

Santos Knight Frank is the first and largest fully integrated real estate services company in the Philippines. Founded by Rick Santos in 1994, he has grown the business to 11 market-leading service lines and over 1,400 professionals across the country. Santos Knight Frank is responsible for more than 4 million sqm of office space transactions, including the largest office leasing deal in Philippine real estate history, and today manages 20 million sqm of property.

The company is part of the Knight Frank global network. Founded in 1896, Knight Frank LLP is the leading independent global property consultancy. Headquartered in London, Knight Frank has more than 16,000 people operating from 384 offices across 51 territories, including the strategically important partnership in the U.S. with Cresa (the world’s largest occupier-focused commercial real estate firm) and Douglas Elliman (leading residential real estate company). For more information, visit www.santosknightfrank.com

If you like this article, share it on social media by clicking any of the icons below.

Or in case you haven’t subscribed yet to our newsletter, please click SUBSCRIBE so you won’t miss the daily real estate news updates delivered right to your Inbox.

The article was originally published by Santos Knight Frank.

More Stories

Vista Land Celebrates 50 Years with Sandiwa: An Event Honoring Leadership, Legacy, and the Filipino Dream of Homeownership

Vista Land Celebrates Love Month in Ilocos Region

Vista Land Bridges Cebuano Heritage and Progress with Valencia by Vista Estates